From the flourishing CTV ecosystem to momentum in linear addressable, the convergent TV landscape was backed by strong tailwinds in 2021.

2020 was a year of remarkable disruption in TV. Consumption habits changed. Connected TV (CTV) viewing exploded. Upfronts shifted and scatter markets swelled. Data and identity were put under the microscope. Many claimed, “what was likely to happen in three years, happened instead in three months.” 2020 brought disruption, and then some.

In 2021, the industry responded. It innovated. It evolved, and in some ways, it returned to normal (or, at least, a new normal). CTV continued to flourish, garnering billions in spend as brands bought-in and the underlying ad infrastructure began to improve. Linear addressable TV took a major step forward, bringing the best of the industry together to rally around common standards and objectives. Data-driven marketing evolved, with alternative flavors of identity and a return to context. And a plethora of new advertisers — big and small, established and disruptive, national and local — benefited from easier access to TV advertising.

2020 was, in a lot of ways, marked by headwinds. By comparison, the media and advertising industry was backed by strong tailwinds in 2021, bolstered by a healthy dose of innovation and collaboration.

To reflect on all of the great developments 2021 has brought, we’ve compiled our top four takeaways from the year in convergent TV, with an eye toward what’s next:

1. With technology and standards in place, linear addressable TV’s last big hurdle lies in interoperability.

2021 marked a major inflection point for linear addressable TV advertising, set to have grown more than 30% YoY when all is said and done. The tone for many in the industry shifted from, “Is this worth doing?” to, “There’s value here. Let’s build, test, and invest.”

Collaborative efforts like OAR and Go Addressable made major strides in establishing consistent standards, while rallying buy-in from agencies, programmers, and MVPDs alike. In the background, technological advancements and pilot campaigns laid the necessary foundation for more advanced testing and scalable applications.

Heading into 2022, the last big hurdle for linear addressable TV lies in making disparate systems interoperable. TV, after all, is very fragmented. There are multiple cable operators, device manufacturers, signaling protocols, and so on. Addressable TV campaigns require a scaled pool of targetable inventory, and, to get there, systems have to work together. Achieving interoperability and meaningful scale next year will require industry-wide collaboration, supported by independent technology and a consistent use of standards.

2. Connected TV (CTV) ad infrastructure is maturing, bringing benefits to programmers, advertisers, and viewers.

As many can attest, CTV viewership has grown considerably over the last 18 months. Streaming now accounts for roughly a quarter of time spent with TV, and this past year saw several exciting developments. A handful of new streaming services were launched. New entrants jumped into the device landscape. And, perhaps even more noteworthy, ad spend in CTV surged — set to eclipse $14 billion by year's end and a whopping $34 billion by 2025.

The CTV ecosystem certainly had a banner year, and behind the scenes, the underlying advertising infrastructure matured in parallel. CTV-focused programmatic technology helped media owners and their ad operations teams better manage advertiser relationships, critical business rules, and, importantly, the experience for viewers.

To give examples, Unified Decisioning technology has helped leading CTV players like Vevo maximize monetization opportunities and deliver premium experiences to both brand partners and users. This includes managing considerations like competitive separation and controlling for ad frequency. The use of ad podding, as another example, has allowed streaming services like Freebie TV to monetize CTV inventory in a more profitable and “TV-like” manner, resulting in significant improvements in inventory yield.

While there is still work to be done in solving issues like bid request duplication and normalizing publisher metadata, the future of CTV couldn't be brighter heading into 2022.

3. Advancements in programmatic advertising technology continue to democratize access to TV inventory for brands.

For as long as it’s been around, TV advertising has been somewhat inaccessible, available only to a select group of prominent brands with sizable budgets. Recent advancements in programmatic technology, however, paved the way for more advertisers to tap into TV and its many advantages: sight, sound, and motion, and a “lean-back” viewing experience. Consequently, a variety of brands — from category leaders to DTC disruptors — jumped into TV and CTV advertising this year, capitalizing on new opportunities to reach consumers alongside the biggest shows, names, and events in television.

What’s more, these developments also changed how many advertisers view and deploy TV. Long seen as a vehicle for reach, TV has undoubtedly become a full-funnel marketing medium, affording brands more strategic ways to engage consumers, to ultimately drive performance.

Over the next year, new advertising applications will continue to emerge as TV becomes more accessible, addressable, and easier to buy.

4. Content metadata and first-party data are becoming essential ingredients for buying and selling media in real-time.

The impending demise of cookies, announced nearly two years ago, spurred tremendous innovation in data-driven marketing over the course of 2021. Alternative identity solutions, such as UID 2.0 and RampID, garnered much of the spotlight. As strong undercurrents, content metadata and first-party data assets also carved out their rightful place in marketing and monetization toolkits.

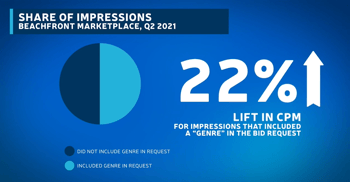

Content metadata certainly isn’t new. Direct-sold TV campaigns have been bought on dayparts and genres, as an example, for some time, while contextual signals have long been used in digital ad targeting. With CTV ad spend increasingly shifting to programmatic, however, this year brought heightened attention to the IAB’s oRTB content object, an often-overlooked specification that helps media buyers and sellers more easily transact on content metadata. Immensely valuable as programmatic and TV converge, the protocol has helped media owners drive premiums in CPM pricing, and provided traders with more campaign transparency.

In addition to context, many advertisers increased their investments on first-party data this year. Publishers and media owners have joined in on the fun as well, with first-party data increasingly ‘becoming a prerequisite for programmatic sales’. Novel applications arose as a result, while innovative tech solutions emerged to help media owners better monetize and protect these valuable assets.

Both of these interrelated datasets — content and first-party — will likely continue to play a bigger role in media transactions next year.

What did we miss?

Drop us a line, here, if we missed any key takeaways from 2021, and if you’re interested in learning more about what Beachfront has planned for 2022.